Canadian First-Time Buyers Start Confident but Lose Optimism at Closing, Ownright Survey Finds

New Ownright survey shows first-time Canadian buyers feel confident early but face confusion and surprise costs during the mortgage closing stage.

2 December 2025 —

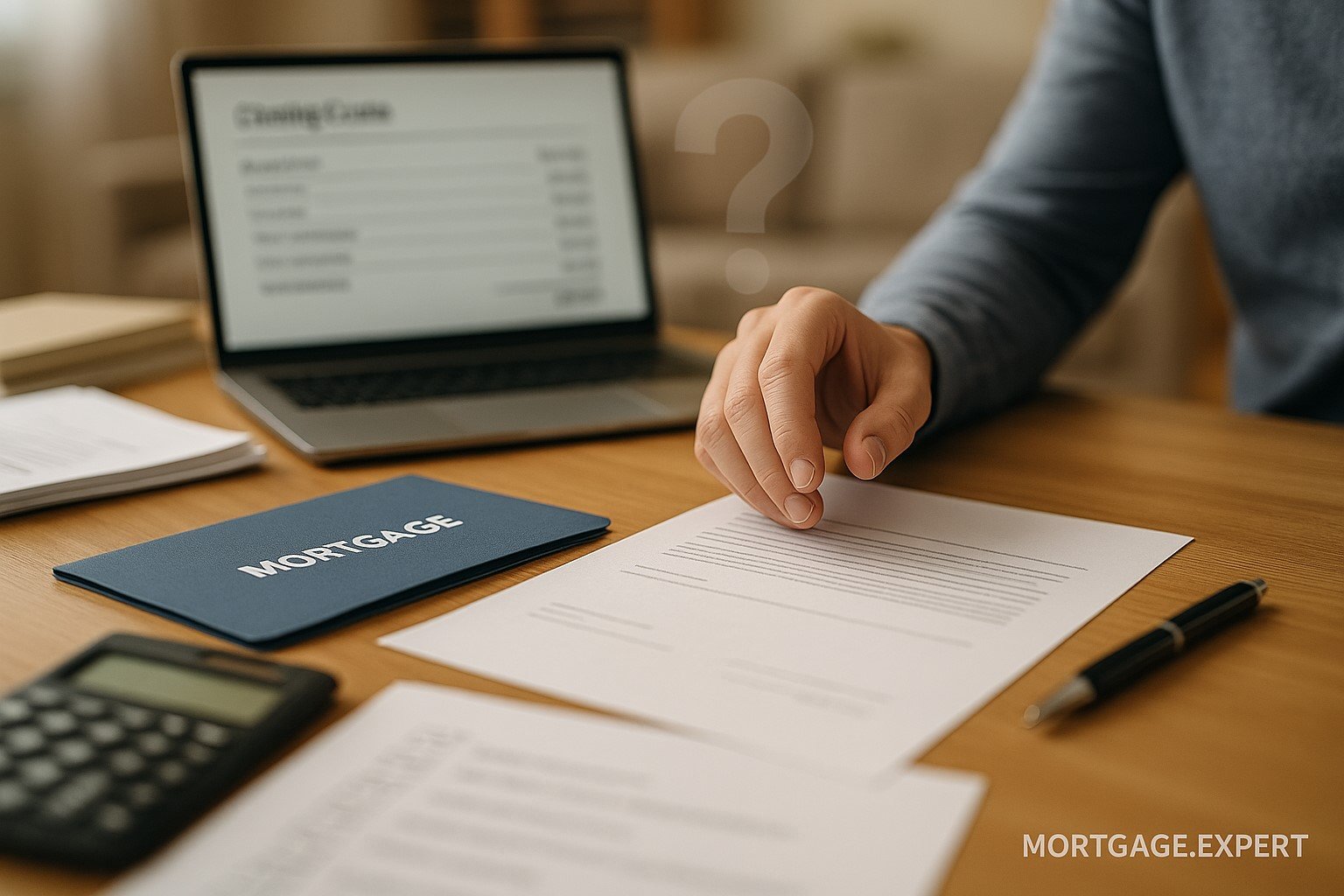

Canada’s first-time homebuyers are entering the market with high confidence but quickly discovering that the final steps of buying a home are far more complex than they expected. A new survey released by Ownright, an Ontario-based real-estate law platform, shows that while homebuyers feel prepared for mortgage shopping, property searching, and budgeting, their optimism drops sharply at the closing stage—the point where legal documents, disclosures, fees, and lender instructions all converge.

The Confidence Curve: High at the Start, Low at the Finish

According to Ownright’s survey, the average Canadian first-time buyer begins the mortgage journey with a strong sense of control. Most respondents said they felt “well-informed and ready” when they started shopping for homes or talking to agents and lenders. Many had researched mortgage rates, understood basic terms like fixed and variable rates, and even compared offers from multiple lenders before choosing one.

But this confidence begins to falter at closing.

Buyers said they encountered unexpected legal fees, lender charges, insurance requirements, land-transfer costs, title search expenses, and municipal charges that had not been clearly explained earlier in the process. The terminology used in closing documents—full of legal language, cross-conditions, undertakings, and lender-specific clauses—left many feeling unprepared and stressed.

A Process Filled With Surprises: What Buyers Reported

Among the most common complaint areas, the survey lists unclear legal terms, late-stage lender instructions, adjustments for property tax and utilities, and title insurance decisions that buyers did not fully understand. One respondent said the closing felt like “a different language, with no translator available,” while another described signing documents they were not fully sure about simply to avoid delays.

Why It Matters: The Pressure of Higher Payments and Renewals

The survey arrives at a moment when many Canadians are already financially stretched. A large number of borrowers with five-year fixed mortgages from 2020–2021 are coming up for renewal at much higher rates. Even though the Bank of Canada’s policy rate—currently 2.25% after cuts earlier this year—has stabilized, many homeowners are still facing significantly higher payments.

In this environment, first-time buyers entering the market are especially sensitive to unexpected costs at closing. When legal and lender documents suddenly introduce additional fees, adjustments, or last-minute conditions, the emotional and financial impact can be substantial.

Legal and Mortgage Professionals Respond

Real-estate lawyers interviewed for the survey said they see the same patterns daily: buyers arriving at closing with incomplete understanding of lender instructions or adjustment costs. Many lawyers pointed out that mortgage pre-approvals often exclude key details that show up only in the final mortgage document package.

The Ownright report suggests several solutions, including earlier disclosure of closing costs, simplified legal language, and better communication between lenders, brokers, lawyers, and clients throughout the transaction timeline rather than only at the end.

Technology Platforms Enter the Conversation

The survey highlights the growing role of technology platforms like Ownright in streamlining legal documentation and explaining mortgage steps in plain language. These platforms aim to offer transparency by giving buyers dashboards that show what costs are coming, when payments are due, and which legal conditions still need to be completed.

Digital mortgage tools and automated closing checklists have gained popularity, but the report states that “the majority of Canadians still rely on traditional law offices and paper-based communication,” which may contribute to slower, more confusing closing processes.

Need Help With Closing Costs?

Mortgage closing in Canada can feel overwhelming — fees, lender conditions, and legal steps often show up late. We explain everything in simple terms.

Talk to a Mortgage Expert

Clara Desai

Articles: 545Related Posts

Stuck with a Mortgage Decision?

Don’t stress — our team is here to help. Reach out for free, no-obligation guidance.

Contact the Experts