Canada’s Mortgage Arrears Edge Higher: CIBC Warns of Early Cracks in Household Credit

CIBC’s Benjamin Tal signals early stress in Canada’s household credit as mortgage arrears climb to 0.24% — the highest in five years. Here’s what it means for borrowers approaching renewals.

Ottawa | 5-Nov-2025, 09:00 EST —

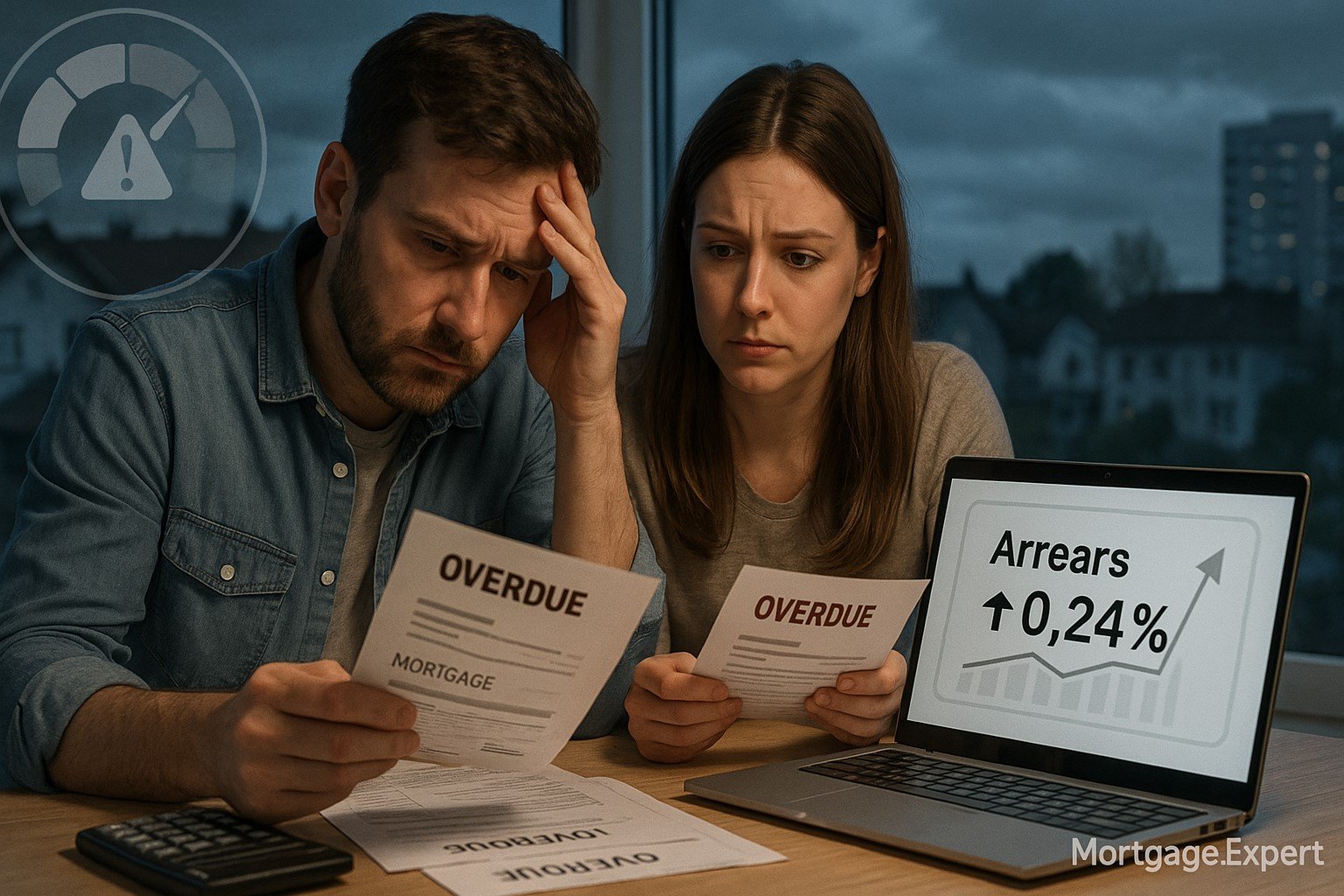

CIBC’s deputy chief economist Benjamin Tal has warned that Canada’s household-credit landscape is beginning to show signs of stress — even as overall mortgage arrears remain historically low. According to data compiled by the Canadian Bankers Association (CBA), the national arrears rate climbed to 0.24% in August 2025, the highest level in five years.

The Big Picture

Tal’s analysis suggests that Canada’s household credit quality — long a source of macroeconomic resilience — is starting to fragment. While most borrowers are still meeting payments, a growing subset of households is becoming vulnerable due to a combination of high debt loads and rising non-mortgage obligations.

“The cracks we’re seeing aren’t a collapse,” Tal said, “but they’re the earliest indication that the next renewal cycle could stretch many borrowers to the edge.”

CIBC data indicate that consumer credit delinquencies — especially on auto loans and credit cards — are rising faster than mortgage arrears. This interconnected debt profile means that households carrying multiple liabilities could face liquidity pressure even before their mortgage resets.

Why It Matters

- Mortgage arrears rising: At 0.24%, the figure is still low by international standards but marks a notable uptick from 0.16% last year. That translates to roughly 1 in 400 mortgages falling behind on payments.

- Higher renewal risks: Roughly 60% of Canadian mortgages will renew by end-2026. Even after the Bank of Canada’s rate cut to 2.25%, many borrowers will face renewal rates 2-3 percentage points higher than their original terms.

- Debt load problem: Average household debt now stands at 179% of disposable income, among the highest ratios in the OECD.

- Regional vulnerability: Prairie and Atlantic provinces have seen the fastest increase in arrears, linked to energy sector slowdowns and softer job markets.

Who’s Most Exposed

Tal points to three risk groups: renters entering ownership through low-down-payment programs, sub-prime borrowers who locked into short terms in 2023, and homeowners carrying significant consumer credit balances. These segments are sensitive to even minor rate changes or income disruptions.

Financial-counselling firms have also reported a spike in clients seeking advice on refinancing and amortization extensions ahead of renewals. This suggests borrowers are proactively trying to avoid default risk — a positive sign for now.

Economic Backdrop

The Bank of Canada’s recent rate cut has not yet flowed fully through to mortgage pricing. Variable rates hover around 5.25–5.50%, while five-year fixed mortgages sit near 5.35%. That means payment pressures remain high even as headline policy rates drop.

Meanwhile, inflation has eased to 2.3%, and unemployment edges up to 6.1%, highlighting a soft-landing scenario that isn’t immune to credit deterioration.

Expert Take

Mortgage analyst Ron Butler notes that many borrowers with “trigger rates” — those whose monthly payments no longer cover interest — remain in extended amortizations with banks. That masking effect may keep arrears artificially low for now.

“The real story will unfold when banks begin to re-amortize loans back to standard terms,” Butler said.

Borrower Takeaways

- Renew early: If your mortgage is up for renewal within 12–18 months, compare options now to lock a rate before further volatility.

- Watch your DTI: Keep debt-to-income ratio below 40%. Refinance high-interest credit if possible.

- Stress test your budget: Run payment scenarios at +200 bps to ensure affordability.

- Consider fixed terms: Stability may outweigh the small premium of fixed rates during uncertain times.

Canada’s mortgage market remains stable on the surface, but micro-cracks in household credit are appearing. The next 18 months — as renewals and higher DTI ratios collide — will test whether that stability holds.

Facing a Mortgage Renewal Soon?

If your mortgage term ends in 2025-26, don’t wait for rates to surprise you. Our licensed advisors can help you compare renewal offers, restructure debt, and lock a rate that fits your budget.

Talk to a Mortgage Expert

Clara Desai

Articles: 545Related Posts

Stuck with a Mortgage Decision?

Don’t stress — our team is here to help. Reach out for free, no-obligation guidance.

Contact the Experts