Mortgage Debt Now 74.5% of Canadian Household Borrowing — A Growing Risk

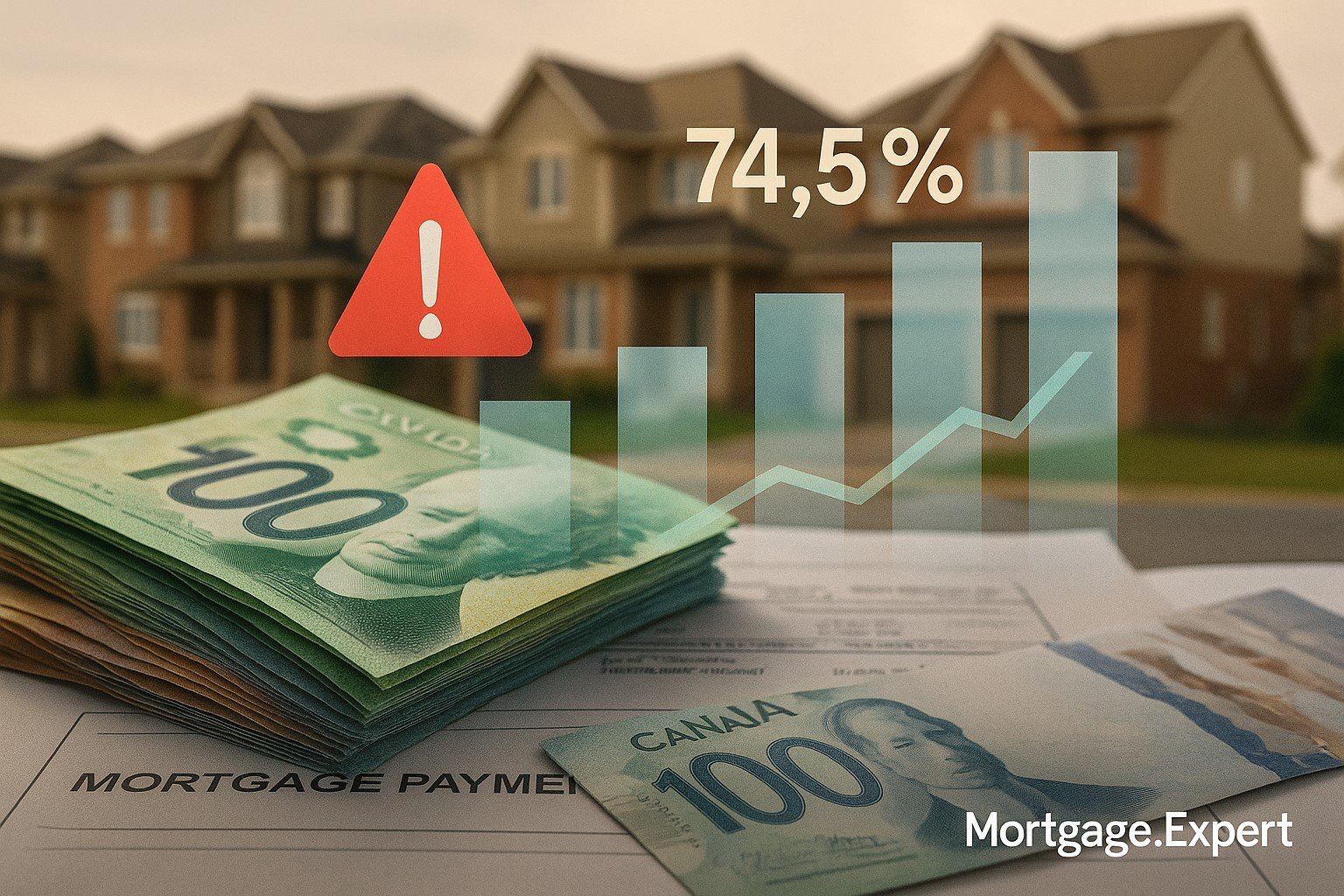

Mortgage balances reached $2.33 trillion in August 2025, now 74.5% of all household debt. Experts warn this concentration could expose Canadians to higher risks if rates or housing conditions shift.

Ottawa | 25-Oct-2025, 11:00 EST — Filed on 22-Oct-2025, 14:20 EST via Kelowna Real Estate Blog

Canadian households are leaning more heavily on mortgage borrowing than ever before. According to fresh data, mortgage debt now makes up 74.5% of total household debt, the highest concentration on record.

What’s Driving the Surge in Mortgage Debt

Several forces have combined to push mortgages to a dominant share of household balance sheets:

- Housing prices: Despite a cooler market in 2024, Canadian home prices remain near record highs, forcing buyers to take on larger loans.

- Renewals at higher rates: Millions of homeowners are rolling over fixed-term mortgages at rates 2–3 percentage points higher than their expiring contracts. This inflates total outstanding balances.

- Population growth: Strong immigration and urban demand continue to fuel homebuying, adding to mortgage demand even amid affordability challenges.

- Slowdown in other borrowing: Credit card and personal loan growth has been more subdued, making mortgages account for a larger slice of total debt.

Why 74.5% Is a Red Flag

Economists warn that such concentration poses risks if housing or interest-rate conditions deteriorate:

- Exposure to shocks: A downturn in housing values would directly hit households’ biggest liability.

- Limited flexibility: With so much income tied up in mortgage payments, Canadians have less room to absorb other cost increases.

- Systemic risk: Banks’ heavy reliance on mortgage lending ties financial system stability closely to housing.

According to the Bank of Canada, about 60% of all outstanding mortgages will renew in 2025–2026, often at higher monthly payments. This amplifies the strain households face.

Mortgage Market Snapshot

| Metric | August 2025 |

|---|---|

| Total Household Debt | ~CAD 3.13 trillion |

| Mortgage Portion | ~CAD 2.33 trillion |

| Mortgage Share of Debt | 74.5% (record high) |

Implications for Borrowers

For Canadians with mortgages, the debt picture highlights both opportunity and risk:

- Equity building: With housing values still elevated, many households have seen net worth rise on paper.

- Payment pressure: At renewal, households face sharply higher monthly payments, cutting into disposable income.

- Borrowing constraints: Regulators like OSFI have tightened lending rules, meaning heavily indebted borrowers may find it harder to access additional credit.

Policy and Market Response

The Bank of Canada’s rate cuts — expected to continue with another reduction to 2.25% on October 29 — may offer some relief to variable-rate borrowers. But experts stress that monetary policy alone cannot address the structural risks of household debt concentration.

Regulators are also monitoring investor mortgages more closely. OSFI has clarified that from 2026, banks cannot “double-count” rental income across multiple properties — a measure aimed at reducing speculative leverage.

Outlook

If rates continue to fall, households could see some easing of payment burdens. However, the sheer scale of mortgage debt leaves little margin for error. Rising unemployment, a housing downturn, or a global economic shock could quickly put households under stress.

Economist Laura Dawson summarized it bluntly: “Canada is more mortgage-dependent than ever. That concentration magnifies risks for families and the financial system alike.”

💬 Worried About Your Mortgage Debt?

If your renewal is coming up or you’re juggling high payments, it’s important to know your options. From refinancing to payment flexibility, our advisors can guide you through the numbers.

Get Personalized Help Now

Clara Desai

Articles: 545Related Posts

Stuck with a Mortgage Decision?

Don’t stress — our team is here to help. Reach out for free, no-obligation guidance.

Contact the Experts