Experts Say Payment Shock Is Coming for All Canadian Mortgages

Mortgage experts warn that nearly all Canadian borrowers—fixed or variable—could face major payment increases over the next 12–18 months. Here's why renewal timing, rising rates, and inflation are converging into a nationwide payment shock.

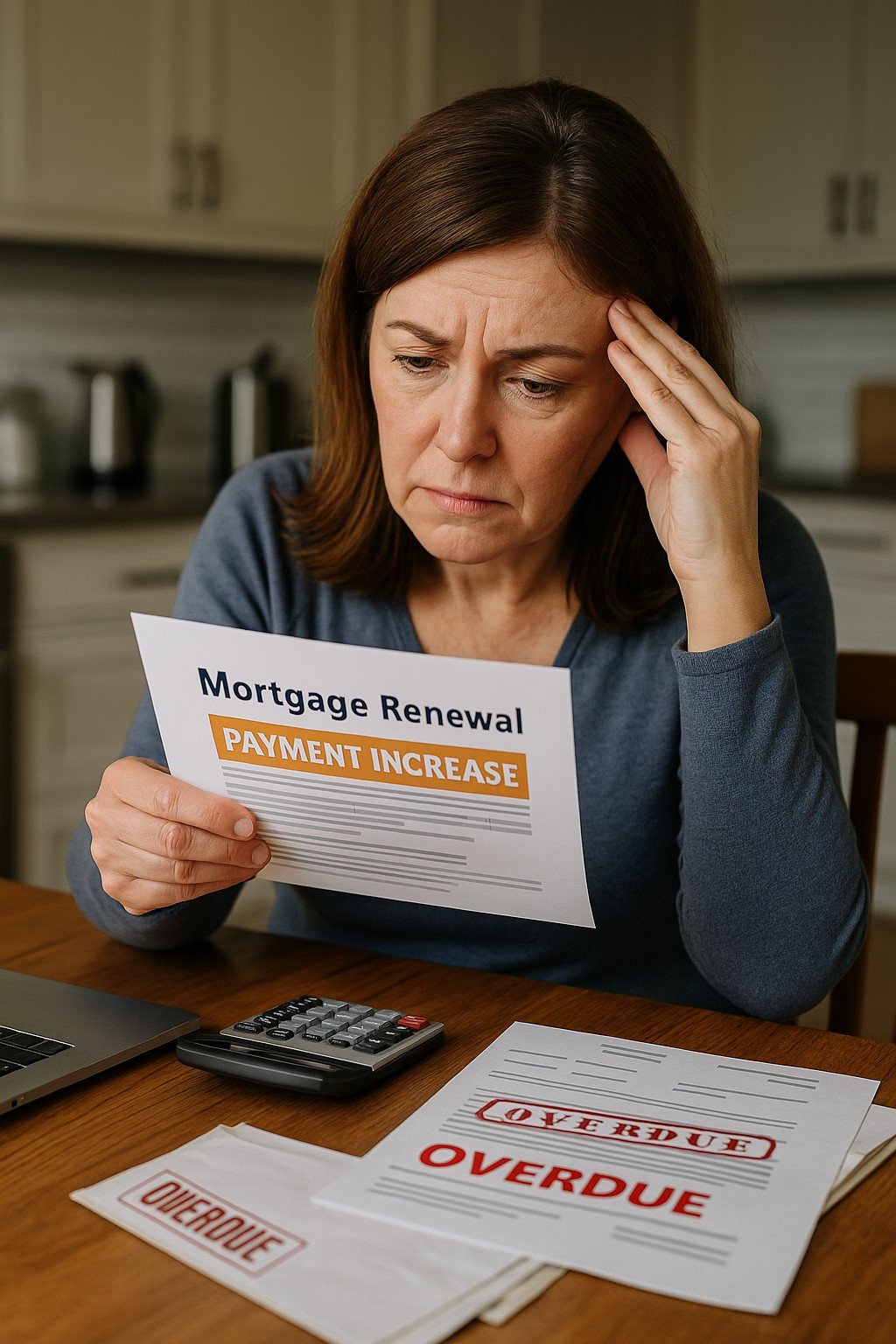

Canada’s mortgage market is staring down a looming challenge — and it’s not just rate hikes. Financial experts and the Bank of Canada (BoC) are warning of a massive “payment shock” awaiting millions of mortgage holders as their terms come up for renewal.

For many, this shift won’t just mean paying a little more each month. It could mean reshuffling entire household budgets to keep up — or worse, facing the risk of falling behind.

The Mortgage Renewal Reality Check

Mortgage renewals are often approached with a mix of relief and dread. But in today’s high-rate environment, it’s more dread than anything else. When fixed-rate mortgages that were locked in at 1.5–2.5% between 2020 and 2021 come up for renewal between now and 2026, borrowers may face an eye-popping increase of 20–25% in their monthly payments.

And it’s not just fixed-rate borrowers. Canadians with variable-rate mortgages are already feeling the squeeze. As interest rates surged, monthly payments for many have climbed dramatically — and in some cases, those payments now barely cover the interest, leaving homeowners with ballooning balances.

Why the Bank of Canada Is Sounding the Alarm

In its 2023 Financial System Review, the BoC placed a sharp spotlight on mortgage debt. The central concern? Households may be underestimating just how much more income they’ll need to maintain their current lifestyle once their mortgage renews.

According to BoC data, the median debt service ratio (DSR) for new mortgages climbed to 19% in 2022 — up from 16% the previous year. Even more worrying is that nearly 3 in 10 new borrowers had a DSR over 25%. That’s the highest this ratio has been in more than a decade.

This rise in DSR means Canadians are putting more of their take-home pay toward housing costs than ever before. And the BoC isn’t mincing words: if rates stay elevated or rise further, the strain could be enough to ripple across the entire financial system.

What Kind of Payment Increases Are We Talking About?

Every mortgage is different, but based on current renewal scenarios:

- Homeowners renewing a 5-year fixed mortgage from 2020 or 2021 may see a jump of $300–$600 per month.

- Variable-rate holders with fixed payments could be nearing or have already hit their trigger rate — where payments no longer cover any principal.

- Borrowers with adjustable payments are already experiencing higher out-of-pocket costs month-over-month.

The BoC projects that by the end of 2026, all mortgage holders — regardless of their product — will face some form of increased monthly payments. For some, this will be manageable. For others, it could be overwhelming.

As mortgage payments climb and renewals loom, softening home prices add another layer of risk — especially for households with minimal equity.

What Can Borrowers Do?

There are strategies to prepare for this payment shock.

- Start budgeting now: Don’t wait for your renewal notice. Use your lender’s or an online calculator (like nesto’s Payment Shock Calculator) to estimate future payments.

- Consider refinancing or extending amortization: If you have equity in your home, you may be able to stretch your amortization to soften the blow.

- Switch to a more flexible mortgage: Explore adjustable-rate mortgages or hybrid products that offer protection with flexibility.

- Consult with a mortgage expert: Mortgage brokers can often find better renewal rates or more suitable products than your current lender.

Don’t Be Caught Off Guard

Your mortgage is likely your biggest financial commitment. With rates holding high and inflation still elevated, being proactive is more important than ever.

Take the time to understand what your future payments could look like. Ask yourself: Can I afford a 20–25% increase? Will I need to reduce other expenses? Should I refinance or switch lenders?

At nesto, our mortgage experts help Canadians prepare for these decisions every day. Whether you’re looking to renew, refinance, or just understand your options better, nesto’s advisors offer unbiased guidance to help you weather the wave of rate changes.

Final Thoughts

Payment shock isn’t just a headline — it’s a real, looming financial hurdle for many Canadian homeowners. But with a bit of foresight, planning, and the right advice, you can cushion the impact.

Facing a Potential Payment Shock?

If your mortgage is coming up for renewal, your monthly payments could jump — fast. Don’t wait for the shock to hit. Get personalized advice on refinancing, switching lenders, or locking in before rates climb further.

💸 Feeling the Pressure of Rising Payments?

Payment shock doesn’t have to catch you off guard. Talk to a mortgage expert today to explore your options and create a plan before your renewal hits.

Talk to a Mortgage Expert

Clara Desai

Articles: 545Related Posts

Stuck with a Mortgage Decision?

Don’t stress — our team is here to help. Reach out for free, no-obligation guidance.

Contact the Experts